What Do Walmart’s and Target’s Results Say About Consumer Sentiment?

Each company had dramatically different results, but it explains an awful lot about the current state of the economy.

Every quarter, I browse through various public companies’ earnings reports to see what is going on outside of my own business bubble. But few reports get me as excited as Walmart and Target. As I’ve explained in a previous article on economic data, most of America shops at one of these two stores. Walmart reports that 90 percent of Americans live within 10 miles of a Walmart branded store (which includes Sam’s Club), while 96 percent live within 20 miles. Seventy-five percent of Americans live within ten miles of a Target. No two companies have a better perspective into consumer sentiment than these two.

Which is why it was perplexing when each company reported vastly different results. Walmart saw its same-store sales increase 5.3% (relative to the same quarter last year), while Target reported growth of just 0.3%. Walmart raised its outlook for the full year to a growth rate of up to 5.1%, while Target expects sales in the next quarter to be flat. Those top-line numbers paint a diverging picture of the American consumer, which means we need to do a deeper dive into each company’s average customer, as well as the details of their latest quarterly results.

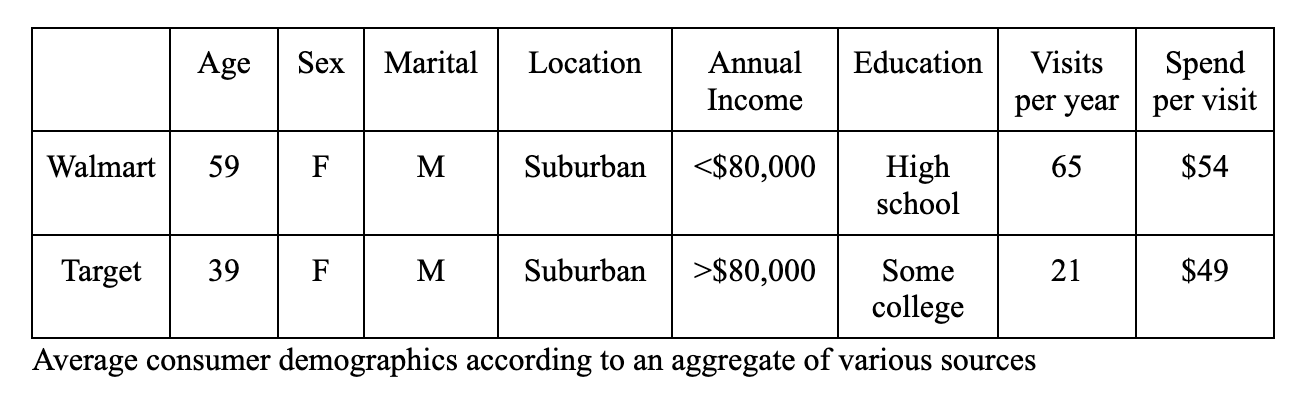

It’s hard to get a completely accurate gauge of the demographics of each company’s customers, but in gleaning data from a variety of sources, it appears that it breaks down like this:

In short, Target’s customers are younger, wealthier, and more educated, while also spreading their total spending around to multiple stores (instead of doing all of their shopping at Target). Walmart customers, on the other hand, seem to do most or all of their spending at Walmart. How does that help us? It doesn’t, just yet, but keep this in the back of your mind as we continue to compare each store’s detailed results. Let’s delve deeper.

Walmart said that the number of transactions rose 3.1%, foot traffic was up 3.1%, and average revenue per order was up 2.1%. Target said that foot traffic was up 2.4% (representing about 10 million more transactions), but average revenue per order was down 2%. Each store stated that they had lowered prices on close to 10,000 items in the previous quarter – Walmart specifically said their prices decreased on average by four percent. Both lowered prices on grocery items in an attempt to give their consumers a bit more cash to purchase discretionary items and saw corresponding increases in the sales of groceries. Both stores also saw a double-digit increase in their e-commerce revenue (including curbside pickup and home delivery).

Those results are fairly similar, so let’s poke around into the details of these two companies’ strengths. Walmart says that 60% of its total sales are in the grocery department. Target says that number is just 23%. That means that Target’s strength is generally in discretionary items that consumers don’t need, while Walmart’s strength is in products that consumers do need to purchase (groceries). This is the biggest difference between the two companies in terms of their operations.

Here’s where the two sides truly diverge. Despite the fact that it is generally a weaker category for them, Walmart said that their sales of “general merchandise” grew for the second quarter in a row after declining for 11 straight previous quarters. And despite the fact that it is generally a stronger category for them, Target says they are in the midst of nine consecutive quarters of “headwinds” for discretionary items. Target CEO Brian Cornell specifically cited “lingering softness in discretionary categories.”

That’s interesting. One store is seeing consumers spend more on discretionary items but the other is seeing a decline in the same category. That’s a big red flag, and so I read a bit further. Walmart didn’t break down their “general merchandise” category, but Target did. They reported that beauty products were up 6%, and their own activewear apparel brand was up double digits. But as a whole, Target’s apparel, home, and hardlines (which includes toys, sporting goods, etc.) categories were all down by low single-digits.

This is where a light bulb went off for me. Target’s private-label apparel (like any store brand) is much more affordable than other apparel brands. And if you’ve been in a Target recently, you’ll know that they have rapidly expanded their beauty offerings. Like every economics lesson teaches, the more competition, the lower the prices. Target shoppers are finding better deals on beauty items because of the variety of options that are not available if you go to a specific brand’s store (or even Walmart).

At this point, my theory was that consumers are spending on discretionary items, but are being extremely picky about what they purchase and where. And as I read deeper into the Q&A section of each company’s earnings calls, that seemed to be the case. Walmart said that their data shows consumers are willing to spend money, but are now much more diligent about doing their research for the best deal they can find. Target stated that, while business was essentially flat, they noticed that the consumer response to promotions was much more pronounced than in previous quarters. Target also mentioned that consumers have veered heavily to purchases of lower-ticket items, specifically in the toy department.

Now, let’s jump back to that demographic chart from earlier. Walmart’s customers historically have lower income than Target’s. But Walmart made a point to mention that 75% of their market share gains this quarter came from households making over $100,000 per year. Who are those wealthier customers that suddenly moved their business over to Walmart? Target customers, of course! That suggests to me that many of Target’s customers began exploring Walmart’s offerings in the hopes of saving some money. Walmart is known to have some of the lowest prices in the country on everything from groceries to clothing. If customers are looking to spend money, but want to be cautious about the bang for their buck, you would expect to see them migrate to a store like Walmart.1

And that makes perfect sense. It is, in fact, good news overall for the progression of the economy as well. For the majority of this year, it seemed consumers were only spending in the parts of their lives they had to – food, rent, utilities, etc. But now, it appears consumers are finally ready to begin opening up their wallets for discretionary items. The only difference is that they’re being much more careful and deliberate in their spending. Sure, to a business looking to maximize its revenue, that’s not good. But looking at the economy as a whole, that to me is a good thing. You want consumers who educate themselves and are willing to do the extra work to ensure they’re making every dollar last. You want to see consumers taking advantage of promotions. You want to see consumers challenging businesses to be at their best.

The economic data of the last few months have suggested things are moving in the right direction. Consumer sentiment hasn’t matched that data, but these earnings reports are the first glimmer of hope that I’ve seen this year. Those of us in business need to always remember to come down off our perches and try to see the world through the eyes of the average consumer struggling to make every dollar last. Average income is up nearly $11,000 (about 19%) since 2020, which is the largest three-year jump since the government began tracking it decades ago. But prices are up about 23% in the same time period. In the last few months, though, it appears that wage growth is finally catching price growth, which would explain why consumers seem to be peeking out of their hibernation dens and testing the discretionary waters.

It’s also, in essence, a “gateway drug.” If real wages are indeed increasing, and if consumers are looking for the cheapest discretionary items, it means the next step is people spending more money on those discretionary items that they have, perhaps, avoided over the last couple years. That may not bode well specifically for higher-priced stores, but it’s a start. Target management and shareholders may not be happy about the recent revelations regarding consumer behavior. But as a neutral party looking at this data, I’m optimistic about 2025.

You would also expect to see customers move to stores like Costco – and wouldn’t you know it, in the last quarter’s earnings results, Costco’s same-store sales were up 4.8%.

Walmart’s success with groceries and value-conscious shoppers versus Target's struggles in discretionary categories really reflects broader economic pressures, that like you pointed out, is starting to shift. The shift in priorities while the economy is in flux is an interesting observation. Do you think Target's investments in premium collaborations or remodels will help them regain footing, or should they refocus on everyday value to stay competitive?