Do You Have Your Priorities Straight as a Business Owner?

Anyone can grow quickly if they do it in an unprofitable way. But most companies can’t stick around for the long term with that strategy.

When someone starts a business, there are a variety of reasons why, as well as a plethora of goals they may be tempted to achieve. Some people want to “change the world” with what they believe is a groundbreaking idea. Some people want to disrupt an existing industry in order to spark greater change. But most people starting a business are looking to simply be successful by providing themselves, their family, and their future employees a means to make a great living.

With so much noise out there, especially when it comes to how you set up your business strategies, to me the biggest question is: what do you want your company’s priority to be? Are you looking to grow quickly and exponentially, no matter the cost? Or are you looking to simply survive in the long run?

To me, the three most important words for a small business are survive, profit, and grow, in that order. To try and succeed in business in any other order seems fruitless, in my opinion. Anyone can grow their business quickly if they do it unprofitably: simply price your goods or services well below anyone else, try to corner your market, and watch your share rise as customers come flowing in. The problem with this is that just about everyone who attempts this will go bankrupt before they ever see true success. Most startups focus on “growth at all costs,” and that cost is usually failure.

This is the famous “Amazon Model.” Amazon was unprofitable for nearly a decade after it first was founded as a small online bookstore in the 1990s. Their strategy was to simply beat everyone on price, which they did for quite a while. They turned their first quarterly net profit in the final quarter of 2001, and their first annual net profit in 2003. But the company continued to lose money in their retail segment (the core part of the business) for many years as they reinvested incredible amounts of cash into their growth. They even raised their prices to the point that Amazon is no longer the cheapest source for goods.1 Even now, while the retail segment of the company is, in fact, profitable, it is so at a very low margin – and the majority of Amazon’s total net profit comes from Amazon Web Services and other high-margin parts of the company.

Amazon’s situation is unique, and there is a reason no one has been able to echo their path to success – and anyone trying to imitate their model is doomed to fail.2 If you’re a business owner who wants your company to have staying power, you need to prioritize accordingly. As Forbes asks, do you want a “costly pursuit of investment and expansion?” Or do you want to “slowly build a profitable foundation?”

Or, better yet, as business consultant Alan Miltz famously said, “Revenue is Vanity, Profit is Sanity, And Cash is King.”

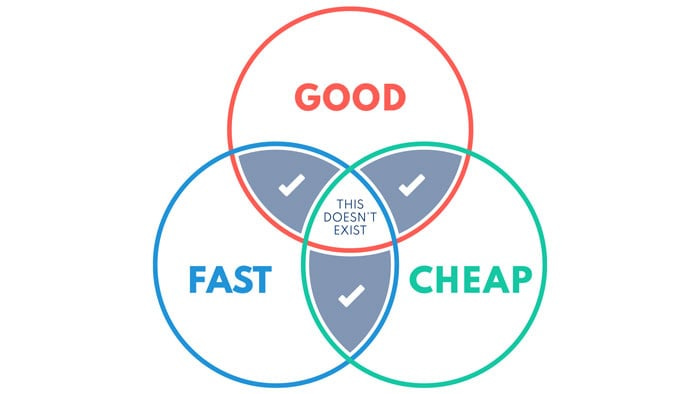

When you set up the strategic direction or corporate culture of your company, you generally have to enter something that has been called the “triangle of trade-offs,” or “the iron triangle.” The triangle’s three points are made up of price, service, and quality. Anyone who tries to choose all three will be unprofitable in the short- and medium-term, and will likely fail without continuous, large capital infusions. It is generally accepted that you can only choose two points with which to run your business. Do you want to be the cheapest option in your market? Then you will have to sacrifice either quality or service. Do you want the best service to sell your high-quality products? That’s fine, but it will be impossible to do that in an inexpensive manner.

Most importantly, there are no wrong ways to set up your business when it comes to which two points to choose from. You can certainly try to be the cheapest – but you need to accept the sacrifices you will have to make on the other side.

Personally, I find that I sleep best at night choosing quality and service for any of my companies. If the biggest knock on one of my businesses is that we are too expensive, I’m okay with that – so long as that same potential customer recognizes that we offer a superior experience and relationship than our competitors. There are a subset of customers that will always look for the best price. That’s perfectly acceptable to me, and there are companies out there that will satisfy their needs. Those aren’t our customers. We are looking for someone who wants to establish a long-term, mutually-beneficial relationship, where we help each other grow and succeed. That costs money. You need to employ a large, high-quality staff, which is expensive. You need to spend excess time (which costs money) on the operations of your company. You have to invest more into your product.

Most existing companies understand this. Despite common belief, the majority of active small businesses are over ten years old. The average lifespan of a business is much shorter than that, but that statistic is skewed. Let me explain: have you ever heard the stat that the average length of a football player’s professional career is only 3.3 years? Usually this stat is mentioned when discussing the effects of injuries, or in explaining why players need to max out their earnings as soon as possible. However, this statistic doesn’t tell the full story. Over 224 players are drafted into the NFL, as well as hundreds more signed out of college, each year. With only 1700 active roster spots available each year, the vast majority of those players don’t make it. So the number of players who play for “zero” years is quite high, and it drags down the average. A more accurate statistic would be, “for anyone who has played at least one season of professional football, the average career is X years.” Unfortunately, no one has ever accurately generated this statistic, though it is believed to be between six and seven years – almost double the statistic that is usually spouted.

Another example: the average human lifespan has increased drastically in the last century. But if you mention to someone how old some of our Founding Fathers were when they died in the 18th or 19th centuries, people are stunned to realize that many of them lived quite long. John Adams was 90 when he died. Thomas Jefferson lived to 83. Benjamin Franklin was in his 80s as well. Charles Carroll, the last surviving signer of the Declaration of Independence, was 95. When you dig into the data, the average lifespan was negatively affected by a very high infant mortality rate. When you have a huge number of humans that didn’t live past “zero,” it drags down the rest of the average. So, while the average lifespan has improved, the age that most humans live to (once they get through childhood) has not really increased that much. What has changed is that we’ve improved our medical knowledge enough to lower the infant mortality rate enormously since the early days of our country.

What does this have to do with business? Remember, 58 percent of existing small businesses are over ten years old. That means that, once a business determines the proper priorities (and doesn’t look to grow revenue at the expense of profit), the majority do last quite a while. Take out all the businesses that start and fail within one year, and the data is suddenly much different than initially reported.3 But you can only do this if you recognize what will cause your business to survive.

There’s a quote that hangs in our office, which has been attributed to Benjamin Franklin: “The bitterness of poor quality remains long after the sweetness of low price is forgotten.” I can’t tell you how many customers tell us that they have to buy from our competitors, but they hate that they have to do so because they love us. I’ve got news for anyone: you don’t have to do anything you don’t want to do in business.4 In my companies, we often make business decisions that harm our bottom line or lose us some revenue. We do so because we choose to run our business a certain way and don’t stray from those principles, no matter the cost. A customer is either looking for the best price or the best service – you generally can’t have both and expect to keep that vendor long-term. We look for the best service ourselves, and thereby provide that same service to our own customers.

Another quote, from 19th century English art critic John Ruskin, sticks in my head when thinking about this topic. He said, “There is scarcely anything in the world that some man cannot make a little worse, and sell a little more cheaply. The person who buys on price alone is this man’s lawful prey.” Now, we didn’t get this far in business by calling potential customers “prey,” and I’m not going to start now. But you understand Ruskin’s point.

My family’s priorities in business have been service and quality, with a sacrifice to price. This has allowed us to succeed as a family business for over half a century. When was the last time you examined your company’s priorities? Make sure, whatever they are, they give you the best chance to last even longer than we have.

Though they have done an incredible job with marketing and public perception, as most people still believe Amazon is cheapest. Amazon is generally not cheaper than everyone else anymore – usually they are about the same, if not slightly more expensive on some items.

There are many people in my niche industry that I’ve watched try (and continue to try) to emulate this model at a very small level and fail miserably – and it is always predictable. If you want to lose money the way Amazon did in order to corner a market, you need to have enough funding that you can last over a decade – but you also need to be in an industry where the size of the pie is enormous. If Amazon had stuck with just books, their model would never have succeeded. They succeeded partially because they tried to corner every market, whose aggregate size was likely in the trillions. Try to name any single market that can be cornered like that. It’s certainly not a small, leisure industry.

There are so many ways to “lie” with statistics, it’s actually quite fun. But that’s a topic for another day.

Except pay your taxes. And your employees. And your vendors. Okay, there are actually a bunch of things you have to do – but just stay with me for argument’s sake.