The Quiet Collapse of the Small Business Advantage

The data show a growing gap between Main Street and corporate America – and it’s unlikely small businesses can keep up.

After the delay of the government shutdown, we finally have economic data from the last few months. And most of it is positive on its face: unemployment remains below 5%, inflation continues to sit at or below 3%, GDP for the third quarter was up 4.3%. Not to mention the stock market, which had its third consecutive banner year. Corporate earnings reports have generally been positive, with continued growth amongst most public companies.

So why does it feel like something’s still off? Talk to anyone on Main Street, be it consumer or small business, and people aren’t feeling too hot. The economy of the last few years has had a plethora of headwinds – inflation and tariffs among the biggest. Larger businesses have hung on just fine. Smaller businesses, on the other hand, are another story.

My grand theory recently has been this: small businesses are falling so far behind the rest of the economy that they are no longer the natural engine of growth in the United States. But since small businesses don’t publicly report their financials, it was nearly impossible to support that hypothesis. That is, until recently.

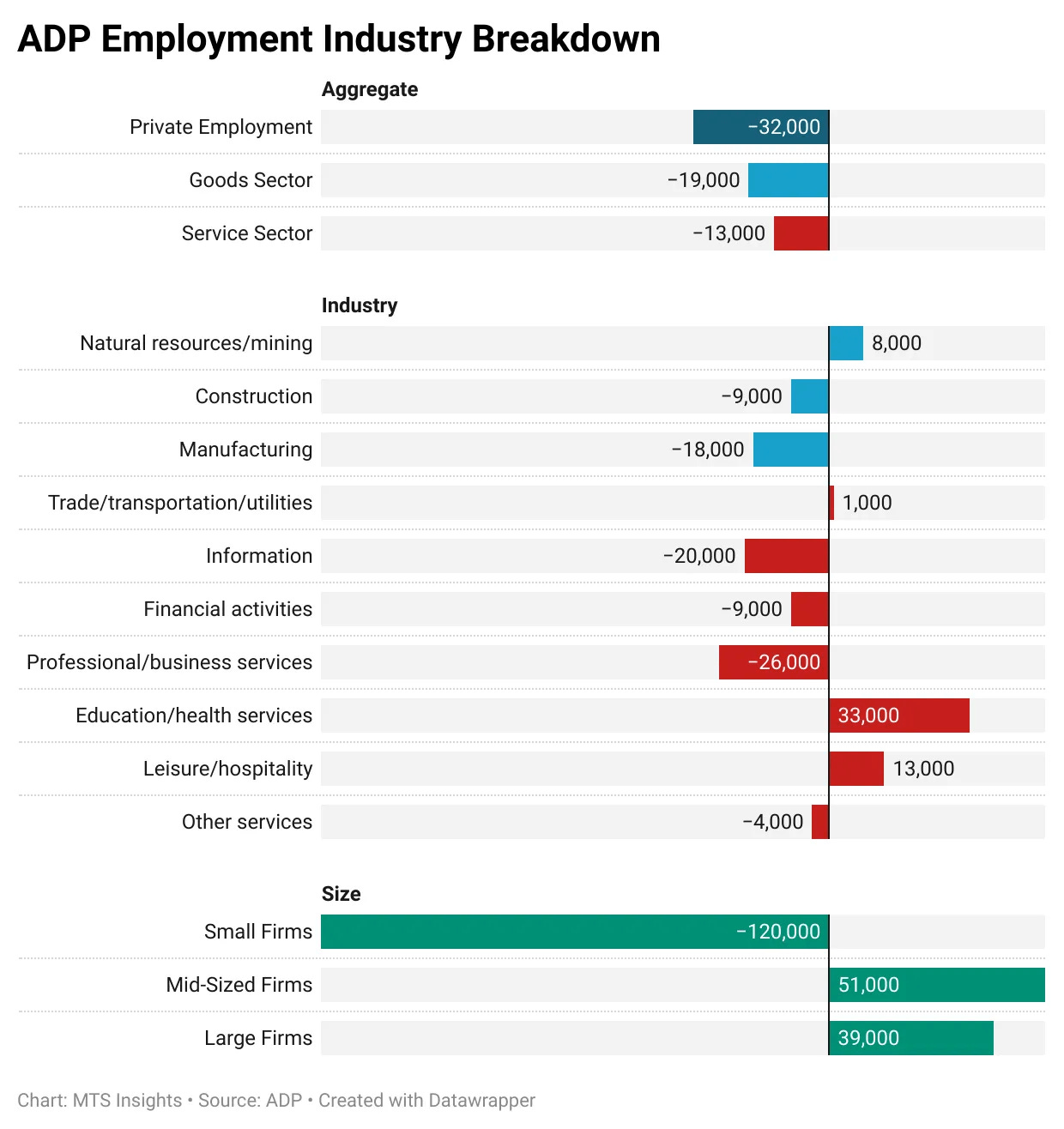

ADP, one of the largest payroll firms in the country, released their monthly employment report and there was a chart that stopped me in my tracks:

These three lines are the change in jobs in the last 12 months. And they show that mid-size and large companies are growing their employment, but among small businesses, defined as those under 50 employees, employment is plummeting.

I delved deeper into their report and it’s as bad as the chart suggests: in November, small businesses cut 120,000 jobs. And private employers (regardless of size) cut 32,000 jobs. Mid-size and larger companies had cumulative job growth of 90,000. That means that almost the entirety of recent job growth has been in large, public companies.

I’m always skeptical of an outlier. So I went directly into the government’s data to see if I could find anything different. And I couldn’t.

The BLS Quarterly Census of Employment and Wages shows that just over 40 percent of jobs are in companies with under 50 employees, a multi-point drop from the historical average. That means over the past few years, the share of jobs that are held by small businesses has decreased significantly relative to its larger peers.

For the life of me, I can’t figure out why this report didn’t get more attention. In my mind, the report should have come with giant red flags and a blaring siren. This is not some niche, marginal group struggling: it’s a core pillar of the U.S. economy, of the labor market.

It’s one thing if the entire economy is weak. If the jobs report is bad all around, or inflation is high, or GDP has stalled. That’s actually easier to explain: economic weakness affects everyone. But this data suggests something far more dangerous: the smallest businesses are losing, while the larger businesses are winning. The economy isn’t generally zero-sum – there’s enough money in the U.S. economy for everyone to succeed. This isn’t a case of all businesses slowing down or being more cautious: this is active divergence based on the size of a company.

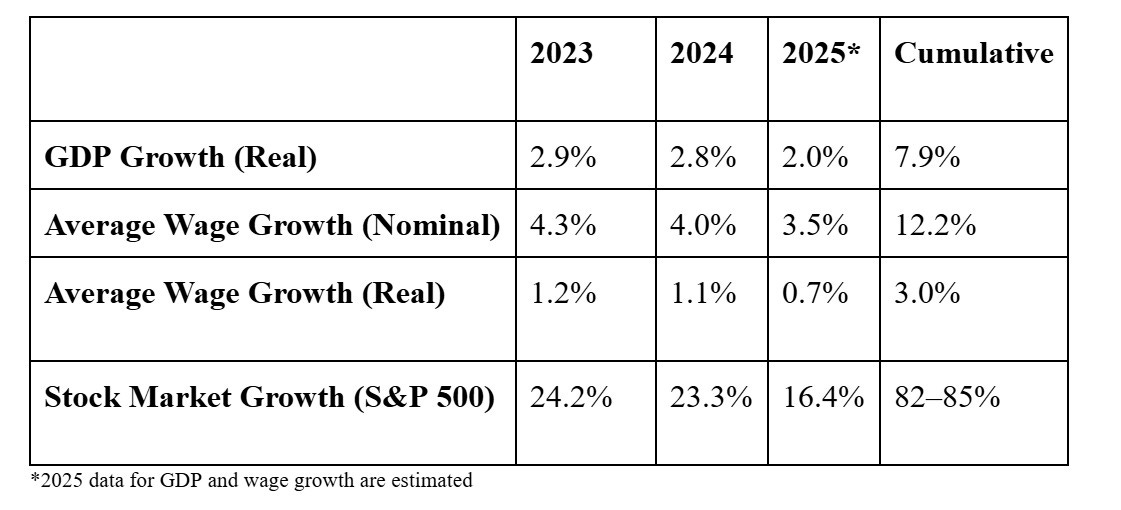

Let’s lay out some of the economic indicators that the government and media use to explain the strength of the economy:

GDP has risen each year. Nominal and real wage growth is up each year. But look at the stock market: in a three-year span, it’s returned a total of nearly 85%.1 That’s only happened one other time since the 1990s.

But here’s the thing: small businesses live in the GDP and wage growth reality. The return of the stock market has little to no effect on those companies, even if they’re invested. Larger companies can leverage that stock market growth in the form of higher pay packages and more valuable stock options/bonuses. They can borrow against their rising equity to help finance their growing costs. Small companies have to rely solely on cash flow. We can’t ask our shareholders or our bank for more money because the value of our company is up. In the small business world, you’re either making money or you’re not.

What has been acknowledged publicly are the skyrocketing fixed costs of running a business. Since 2023, commercial liability insurance is up about 15% on average. Utilities are up more. Payroll costs are up the same amount. Software costs are up around 20%. Employer-sponsored healthcare plans have increased about 25% on average.2

Amidst these rising costs, as well as general inflation that has peskily stuck around since 2021, small businesses can’t keep up. Larger companies can squeeze suppliers or even absorb margin hits. Small businesses generally have to say “yes sir, may I have another.” Larger companies can hire into uncertainty. They can hire and fire at will. If they get into a bind, they can cut some jobs or issue another corporate bond. Small companies can’t miss payroll even once. Small companies can’t pump revenue up in the same way larger companies can. Fixed costs go up regardless of your revenue – that’s the nature of the cost being fixed in the first place. And when fixed costs rise this much, this fast, it’s nearly impossible for revenue growth to match it.

Now, there’s no data that suggests small businesses are closing at any greater rate than businesses of any other size. But it means that the game is changing. It means the definition of success is changing. Growth at all costs is rarely a strategy that works for small businesses in the best of times. It certainly won’t work when the deck is stacked against you.

So, if small businesses are cutting jobs, but still remaining in business, it suggests one of two things: first, that business is down everywhere. I don’t buy that, because again, the data doesn’t support it. The second option is that small business leaders are opting out of scale. They’re choosing not to hire people when they might have otherwise. They’re choosing not to replace an employee that leaves or retires. They’re choosing not to take on more risk. If your fixed costs are up that much more than your revenue, you have no choice but to skimp on your variable costs. That means decreasing payroll, lower-margin products and services, building upgrades, software upgrades, and anything else that can be pushed off another year. Small businesses are opting out of growth because growth has become too expensive.

If you’re in the small business world, you’ve probably heard people complain that it takes way more work to do the same amount of business. There are a variety of reasons behind that: business ownership has gotten way more complex in the last decades; increased regulations have made compliance much harder and more costly; and some owners are simply taking on more tasks themselves to avoid having to expend cash hiring an extra person or two.

I’m not looking to be a Debbie-Downer. In fact, I don’t think this is even an existential risk to small businesses: most family-run companies can adjust to a changing landscape accordingly and survive just fine. This data isn’t suggesting that small businesses are collapsing. Rather, it shows that they are showing quiet restraint and simply acknowledging that the rules have changed. There is a widening gap between Main Street and corporate America, and small business owners know there’s pretty much nothing they can do to change that.

Perhaps we just need to reanalyze what we consider success for a small business. There are pundits every day who declare the American Dream dead, but that’s clickbait. The American Dream is alive and well, though the route to get there certainly has some detours. Just because small businesses don’t seem as successful when we use the same metrics we’ve always used, doesn’t mean we suddenly won’t have small businesses. But we do need to begin adjusting how we view their role in the modern economy, especially if we want to ensure that they’re indeed here in the future.

Unfortunately, I don’t have a solution. I don’t have some inspirational words or a magical fix. There isn’t a policy tweak or a productivity hack that closes this gap. The forces that drive this change are structural to our economy. I would argue that being a small business owner has never been harder than it is now. And business is supposed to be hard. No reasonable person ever asked for it to be easy.

But we’re entering new territory now. We’re in a society where the public as a whole seems to be okay with small businesses being left behind. Everyone says they want to support small businesses, but when they have to tighten their purse strings, they understandably migrate to Walmarts, Amazons, and Costcos. I don’t blame them – I would do the exact same thing. No one looks out for you better than yourself.

The danger isn’t that Main Street disappears. Rather, it’s that we keep pretending we can continue to succeed using the old playbook. The danger is in doing the same thing we’ve always done, and expecting the same result. Times have changed, and sometimes you can do everything correctly, and still fall behind.

Whether this shift is a long-term problem or simply a rational evolution of a global economic superpower is yet to be seen. We’ve lived through major economic transformations before – the industrial revolution, the dot-com era, and now the rise of artificial intelligence. And we’ve always come out the other side. But each of those major shifts in society still produced long, uncomfortable periods where entire groups got left behind.

Small business owners aren’t suddenly less capable or less driven. Rather, they’re responding rationally to an environment that now rewards scale, capital access, and risk absorption in ways they simply can’t match. The real risk isn’t that small businesses disappear; it’s that we continue to judge them by outdated measures, expect them to control the things they can’t control, and fail to recognize that sometimes the smartest move in a changed system is not to grow at all.

Congrats, Bezos!

And in my experience, I’d have been thrilled with a healthcare increase of just 25%...